#Finance101: 3 red, green and beige flags...

When it comes to money matters

Whether we like it or not, it is growingly inevitable that more companies will adopt AI technologies in the workplace (if they haven’t already).

But instead of fearing unemployment, what if we asked: "How can I work with AI to improve my capabilities?"

Start working with, not against AI with these three actionable tips

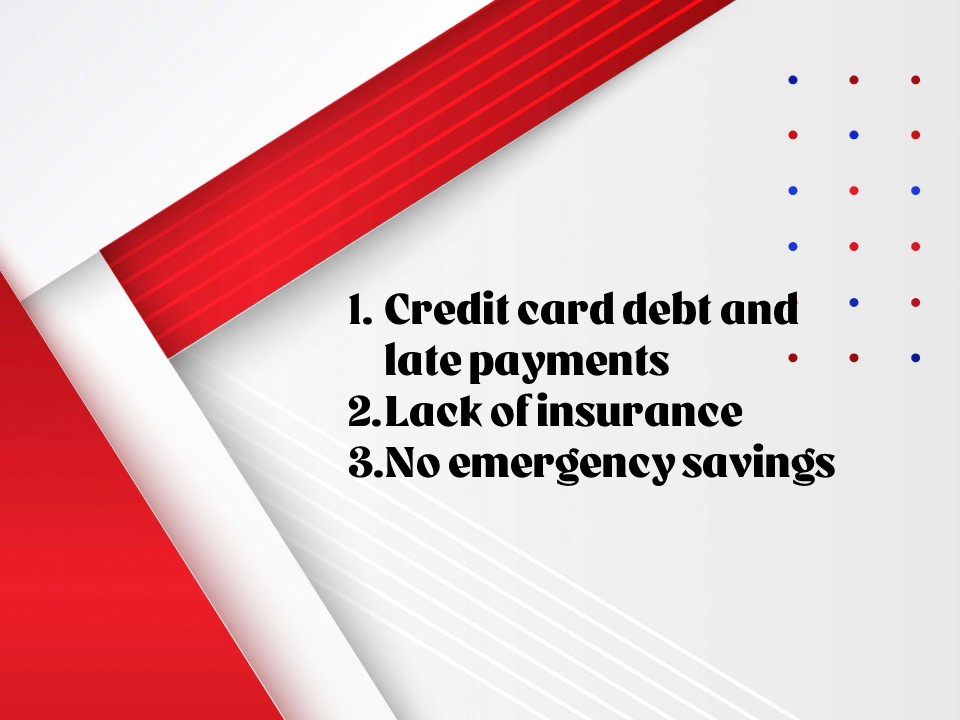

Red flags

Green flags

Beige flags

We all know what red flags and green flags are when looking for a romantic partner.

Some of these flags are painfully obvious – overly controlling behaviour and anger management issues are clear red flags, while self-awareness and respect for boundaries would be considered green flags.

But when it comes to money matters, these flags may not be so obvious, so here’s our very own list of red and green flags to look out for when it comes to money matters.

Let’s start with the Red Flags first…

- Credit card debt and late bill payments

This is arguably the biggest red flag in personal finance.

Why? Because the interest rates charged by credit cards are exorbitantly high!

In addition, the late charges for credit cards can be over $100, regardless of the amount outstanding. That’s a steep price to pay, especially when one could’ve arranged for automatic GIRO payments or simply paid the minimum amount on time (usually no more than $50).

- Lack of insurance

Being underinsured is extremely dangerous and is a huge red flag! This is especially true if you’ve been working for a couple of years and can afford to buy protection policies.

Why? Because should something serious happen to you, the last thing you would want is to be a financial burden on others. Getting an appropriate amount of coverage via protection plans goes a long way in mitigating this red flag.

- No emergency savings

Life is unpredictable, and unexpected expenses can arise at any moment. An emergency fund serves as a financial cushion to help you cover costs like medical emergencies, sudden laptop repairs, or unexpected unemployment. Without an emergency fund, you may end up relying on credit cards or loans, leading to debt and worsening your financial situation.

Financial experts typically recommend having at least three to six months' worth of living expenses saved up in a liquid, easily accessible account.

Now, on to the Green Flags…

- Budget planning

Just having clarity on how much you spend every month on essentials and non-essentials, will help you justify making some changes to your lifestyle where necessary, especially if it allows you to save more regularly.

- Regular savings

Being able to set aside a portion of your income regularly is key. It demonstrates the willingness to prioritise your funds responsibly and serves to build up and maintain an emergency fund, as well as opens opportunities for investments in the short- and long-term.

- Diversified investment portfolio

While we all have differing risk appetites and may prefer some assets over others, diversification gives us the power to ensure that our investments keep pace with inflation. Finding that balance between risk and reward isn’t always easy, but at least having a less volatile portfolio will go a long way in ensuring a healthy and secure retirement.

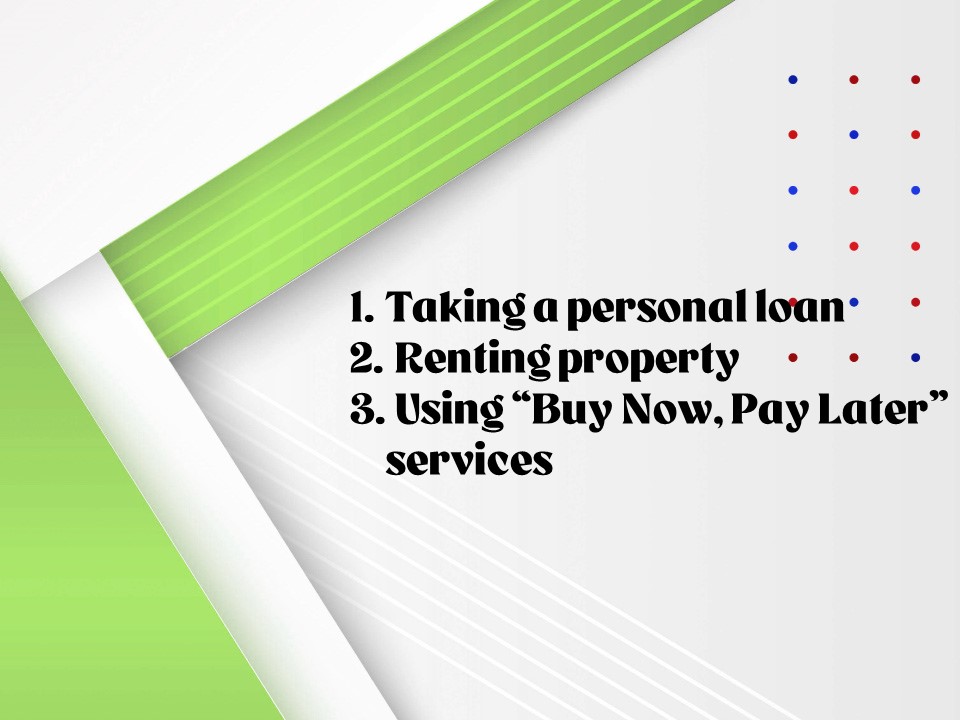

… But what about ‘Beige Flags’?

In case you missed it, there’s a new trend called “beige flags”, which is neither a red flag (i.e. a trait to be avoided) nor a green flag (that is, an indicator of a healthy financial situation).

Here are three beige flags we’ve identified.

- Being in debt

Debt might come with a bad rep, but it’s not a red flag! Being in debt is not inherently bad; it's about how and why you incur it.

For example: It’s normal to take a loan to pay for housing or education – both of which are huge expenses that will affect your cash flow.

That said, getting into high-interest credit card debt, or using debt to fund unhealthy habits such as gambling or a lifestyle you can’t afford are clear red flags.

- Renting property

One common perception about renting is that it's just ‘throwing money away’. Well, not exactly. Renting can offer flexibility, especially if you're in a transitional phase of life – or are not sure whether you want to settle down in a location yet.

Depending on your rental agreement, it may also free you from the responsibilities and costs of property maintenance, which are typically covered by the landlord.

Remember, both rental and property ownership have pros and cons! Ultimately, analysing which is “better” depends on your lifestyle preferences, your need for mobility and your overall financial situation.

- Using "Buy Now, Pay Later" services

While “Buy Now, Pay Later” (BNPL) services have quite a bad reputation for encouraging impulse buying and spending beyond one’s means, they’re not necessarily a red flag.

Why?

Well, these services can help make more significant purchases manageable by breaking them down into smaller payments. Ultimately, BNPL is a financial tool, and it is the user that determines whether it's used responsibly or not.

Spot any of these flags on yourself? Do a financial health check today!

Wealth insurance

Includes SRS investment, capital guaranteed, endowment, investment-linked, lifetime payout

{kind=link}

Let us match you with a qualified financial representative

Our financial representative will answer any questions you may have about our products and planning.